Leasing & Hire Purchase

Conceptually a lease may be defined as

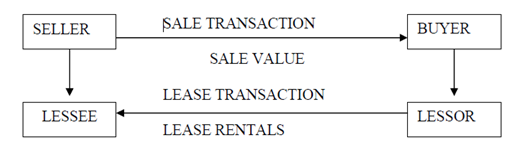

- A contractual arrangement in which a party owning an asset (lessor)

- Provides the asset for use to another (lessee)

- For an agreed period of time (lease period)

- For consideration in form for periodic payments( lease rentals)

At the end of the Lease period, the asset reverts to the lessor unless there is a provision for renewal of contract. Thus leasing is a device for financing the cost of an asset. The lessor does not take recourse to the asset as long as the rentals are regularly paid to him.

Advantages of Leasing:

To the lessee:

- Financing of asset up to 100%.There is no need of making any down payment, company is able to start his business straightaway.

- Funds are not blocked of the lessee; the same can be used for some optimum use.

- Leasing provides finance without diluting the ownership or control of the problems unlike equity or debt.

- It is preferable to Institutional Finance as restrictive covenants such as representation in the board, conversion of debt or equity, payment of dividend etc. are absent.

- Facility to structure the lease rentals according to his business operations and his paying capacity is another major advantage for the lessee.

- Simplicity of the lease finance arrangement at mutually agreeable terms.

- In a leasing arrangement the risk of obsolescence rests with the lessor and the lessee always has the option of replacing the asset with latest technology.

- By employing ‘Sale and Lease back' arrangement, lessee may overcome a financial crisis by immediately arranging financial resources.

To the Lessor

- Lessor's interest is fully secured as he is always the owner of the asset and can take repossession of the asset is the lessee defaults.

- Higher Profitability since rate of return is more than in case of lending business.

- Leasing business has a high growth potential.

Disadvantages to lessee:

- Restrictions on use of leased equipment : for example, lessee would not be permitted to make additions on alterations to suit his needs.

- A financial lease may entail a higher payout obligation , if the equipment is not found useful subsequently and the lessee opts for premature termination of the lease arrangement.

- Lessee mostly never becomes the owner of the asset and is thus deprived of the residual value of the asset.

- Consequences of default may prove costly for the lessee.

- Since leased assets do not form part of lessee's assets they do not appear in his balance sheet and thus understates his assets.

Types of Lease :

The lease agreement can be classified into following categories:

1. Financial Lease:It is a lease, which transfer all risk and reward of ownership of an asset to the lessee by the lessor but not the legal ownership. The lessee selects the assets the equipment, settle the lease rental and lease period and can also go for purchase option, where at the end of lease period, the lessee has the option to buy equipment at a predetermined value. The finance lease may also contain a non- cancellable clause which means that lessor transfers the title to the lessee at the end of the lease period.

The lessee uses the equipment uses exclusively, insures and maintains it. It also bears the risk of obsolescence. Contractual period between lessor and lessee is generally equal to full expected economic life of the equipment.

The Financial lease is very popular in India as in other countries like USA, UK, and Japan. High cost equipment such as machinery; diesel generators aircraft, land and building are leased under finance lease. The assets leased are generally of specialized nature.

2. Operating Lease: In this lease, the contractual period between lessor and lessee is less than full expected economic life of the asset. The lease is for a limited period of time may be a month, six month, a year or few years. Normally, the risk of obsolescence is enforced on the lessor who will bear cost of maintenance, insurance and other relevant expenditure.

The lease is suitable for (1) computers, copy machines and other office Equipment, vehicles, material handling equipment which are sensitive to obsolescence (2) where the lessee is interested in tiding over temporary problem

3. Sale and Lease Back: Under this type of lease, a firm which has an asset sells it to the leasing company and gets back on lease. The asset is generally sold at its market value. The firm receives the sale price in cash and gets the right to use the asset during the period of lease. The firm makes periodical payment to the lessor. The title to asset vests with the lessor. Sale and lease back is done generally in case of airline industries.

4. Leverage Lease: There are three parties to the transaction: (1) Lessor (equity investor), (2) Lender (Bank or FI), (3) Lessee. Under Leverage lease arrangement, the lessor borrows a substantial borrow the purchase price of the asset from the lender which is typically a commercial Bank or financial institution. The lender obtains an assignment of the lease and rentals to be paid by the lessee and insists on first mortgage on asset.

5. Cross Border Lease: Cross border lease is also known as international leasing, export leasing, and transnational leasing. It relates to lease transaction between lessor and lessee domiciled in different countries. In other words lessor may be in one country and lessee may in other country. To illustrate, if a leasing company in USA leases machinery to a manufacturer in India.

Distinguish between financial lease and operating lease:

1. In financial lease the lease period is generally for economic life of the asset, therefore in life of the asset there will be one lessee. In operating lease the asset is for a shorter period says a month, six month, a year or few years, therefore there are many lessees in the life of the lessee.

2. Financial lease is suitable for high cost equipment such as heavy machinery, diesel generators, aircraft, land and building are leased under finance lease. The assets leased are generally of specialized nature. The operating lease is suitable for (1) computers, copy machines and other office Equipment, vehicles, material handling equipment which are sensitive to obsolescence (2) where the lessee is interested in tiding over temporary problem.

3. In financial lease, the risk of obsolescence is assumed by lessee. In operating lease, risk of obsolescence is borne by the lessor.

4. In financial lease contracts are usually non-cancellable, whereas in operating lease contracts are cancellable.

5. In financial lease maintenance cost, insurance are generally borne by the lessor. In operating lease maintenance cost, insurance are generally borne by the lessee.

6. The idea of financial lease is to finance the asset. Operating lease is a true rental concept.

7. Accounting treatment discussed below. : In case of finance lease the fixed asset are recorded in the books of Lessee and in case of operating lease the lessor.

Hire purchase:

In a hire purchase transaction the goods are let on hire by finance company (creditor) to the hire purchase customer (hirer). The buyer is required to pay an agreed amount in periodical installments during the given period of time. The ownership remains with the creditor and passes on to hirer on payment of last installment.

Features of Hire purchase Agreement:

- In hire purchase, hire purchase customer the takes the possession of goods immediately and agrees to pay hire purchase installments for an agreed period of time.

- The ownership of goods is passed to the hire purchase customer on payment of last installment.

- If there is a default in any one installment, the seller is entitled to take the goods back.

- The hire purchase customer has a right to terminate the agreement at any time before the property passes. Thus he has an option to return the goods in which case he need not pay the installments falling due thereafter. However, he can recover the sums already paid as such sums legally represent hire charge on goods in question.

Contents of Hire purchase Agreement:

There is no prescribed format for a hire purchase agreement, but it has to be writing signed by the both parties to the agreement.

A hire purchase agreement must contain the following particulars:

- Description of the Hire purchase customer and creditor.

- Description of goods in a manner sufficient to identify them.

- Details of hire purchase installment i.e. number of hire purchase installments, amount , due date of payment.

- Arbitration procedure in the event of dispute.

Hire Purchase and Credit Sale:

Hire purchase is different credit sale, because in credit sale. In credit sale, the ownership in goods is passed the buyer immediately, where as in case of hire purchase it is transferred on payment of last installment.

Hire purchase and Lease:

| Lease | Hire purchase | |

|---|---|---|

| Ownership | Lessor is the owner and the lessee is entitled to economic use of asset. Lessee never becomes the owner of goods | Hire purchase customer becomes the owner on payment of last installment |

| Depreciation | Charged in books of lessor in case operating lease and in case of finance lease in the books of the lessee. | Hire purchase customer is entitled to claim depreciation. |

| Magnitude of Funds | Magnitudes of Funds involved are usually large. | Magnitudes of Funds involved are comparatively less. |

| Maintenance | In finance lease the lessee bears the cost of maintenance, where as in operating lease, lessor bears cost of maintenance | Hire purchase customers have to bear cost of maintenance. |

| Tax benefits | Lessor is allowed to claim depreciation and lessee is allowed to claim tax benefits on rentals and maintenance cost. | Hire purchase customer is allowed to claim depreciation and finance charge. Seller may claim interest on borrowed funds to acquire the asset for tax purposes. |

| Extent | Lease financing is invariably 100% financing and no payment of margin money/ down payment/ deposits are involved. | In a hire purchase transaction margin money equal to 20-25% may be payable and at times deposits are collected by finance company repayable after payment of last installment. |

- CA. CS. CMA. MBA. - Naveen Rohatgi